I can sometimes look back and remember some of the benefits that my corporate job once gave me, with the main benefit being a sense of security and certainty. It was nice to know I had a consistent paycheck coming from week-to-week. Yet I wouldn’t trade my business for that life again, and I’ll tell you why.

For one thing, entrepreneurship gives me so much flexibility. It’s what’s allowed me to create the life I had always imagined for myself. (Learn more about aligning your business with your vision here). For another, it’s possible to mitigate risk and build security as an entrepreneur. The secret? Being proactive.

You can take control of your business and do your best to insulate it from the unexpected (like a pandemic or a recession) by focusing on three crucial aspects of your business that are essential to its success. They are your health, your finances, and your clients.

Without your health, you can’t run your business to its full capacity. (Find out more about self care as a business owner here).

Many business owners have been faced with this fact during the coronavirus outbreak. When you’re sick or burnt out, you can’t deliver the same quality of services. We all know the basics of maintaining your health like eating a variety of fresh foods and staying active but there are a few particular tips to keep in mind as a business owner. For instance, you should create clear boundaries between work, life, and your clients in order to keep the balance. I would also suggest taking advantage of your open schedule and allowing yourself to take a break from time to time during the day.

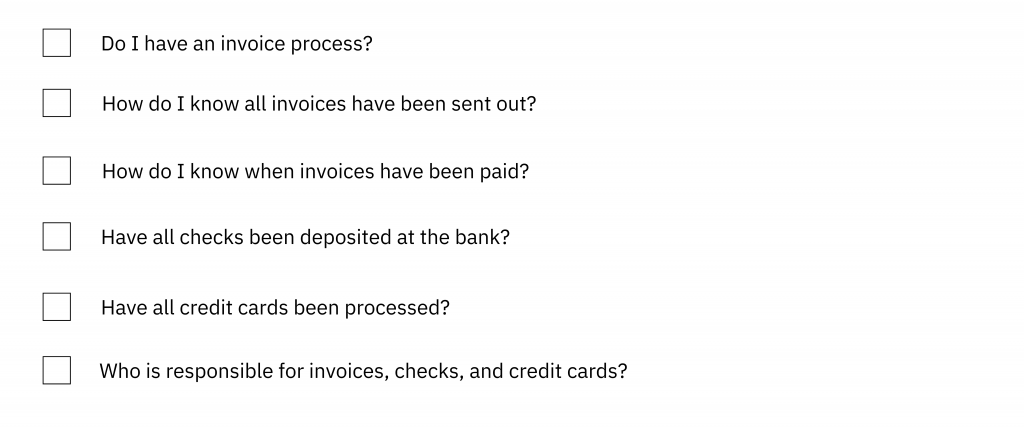

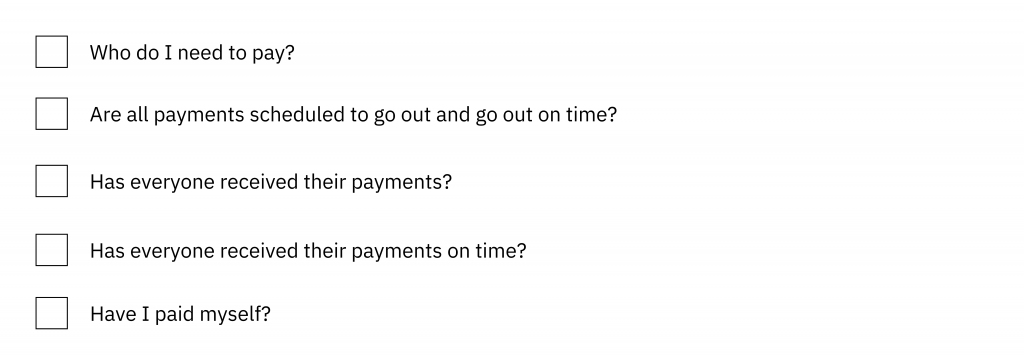

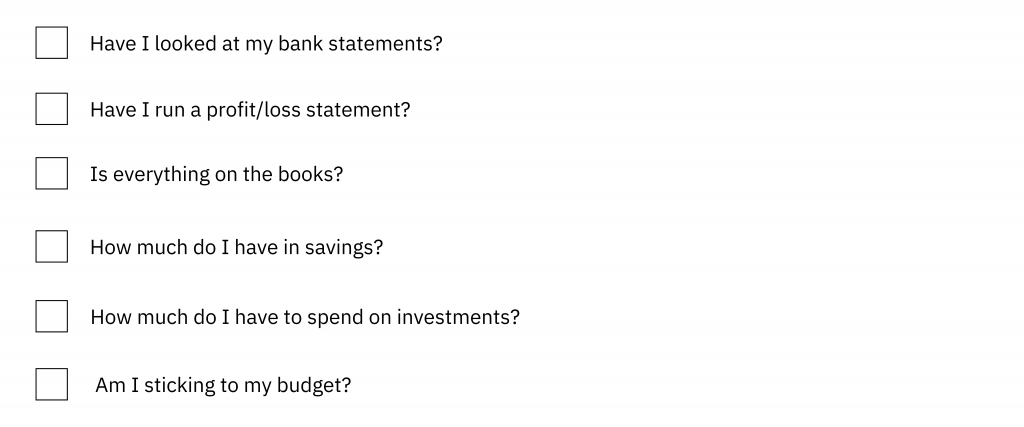

Maintain your finances because cashflow is what keeps your business afloat. (Read more about maintaining your finances here).

To be diligent with your finances is to be strategic about your money moves, set aside funds for emergencies and other unexpected circumstances, and keep a budget that gives you the agility to change course at a moment’s notice. (Get the small business budgeting guide here). If your original business plan isn’t bringing in the same profits, you have to have the funds available to pivot over time.

You couldn’t maintain a business without clients so reach out to them early when there are signs of changing times.

Towards the start of lockdown, I checked in with all of my clients and evaluated where they were at. Many of them were struggling and didn’t know what to do. Thankfully, I could see more clearly from an outside perspective what changes they’d be able to make in order to keep their business going. As they continued to make profits, they were able to continue to stay on as clients.

The longest lasting entrepreneurs I know are proactive instead of reactive. Focus on maintaining your health, finances, and clients, and your business can survive anything. Something else that will help you survive, and even thrive? Working with Mitchell Consulting. Fill out our questionnaire to make sure we’re a good fit.

You want to scale your business but that’s going to require a lot more money. What now? You can breathe easy because you’ve got options.

You want to scale your business but that’s going to require a lot more money. What now? You can breathe easy because you’ve got options. You can hire all the accountants, bookkeepers, tax strategists, all the financial professionals in the world to take care of your business finances but nothing will fully exempt you from being involved.

You can hire all the accountants, bookkeepers, tax strategists, all the financial professionals in the world to take care of your business finances but nothing will fully exempt you from being involved.